Offset VS Redraw Which is better ?

This is a question that as mortgage brokers in Sydney we get asked all the time by home buyers, so I thought I would break down how they work, the differences and I will dispel some myths around offset and redraw accounts.

The short version:

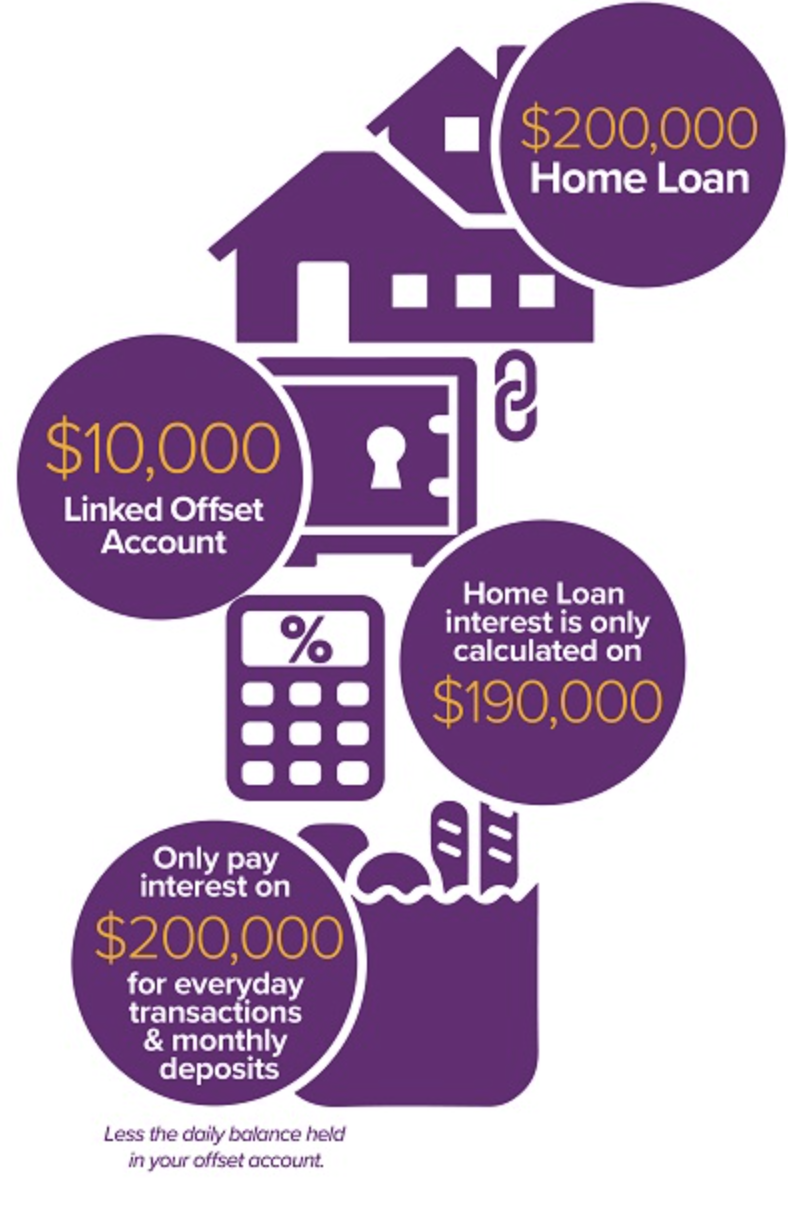

An offset account is a transaction account linked to your home loan, reducing the balance on which interest is charged and thereby saving you interest. In contrast, a redraw facility allows you to access extra payments you’ve made on your home loan.

Offset accounts and redraw facilities both lower the amount of interest you pay on your home loan by reducing the balance.

With a redraw facility, you save on interest directly, as the extra payments you’ve made (and can withdraw if needed) decrease your loan balance. An offset account, on the other hand, indirectly saves you interest because the lender calculates your home loan interest based on the loan balance minus the balance in your offset account.

The breakdown:

What is an offset account?

We always recommend saving money to our clients, I know this is a pretty basic piece of advice, however you will be surprised how many people we come across who live pay check to pay check or they are not planning for their future.

So how does an offset help with this? Well if you have a home loan or are planning to get a mortgage, an offset is the best savings account you will ever have.

Whilst most people are focussed on high interest accounts which usually pay you a measly amount (especially these days) and have to pay tax on, an offset saves you from interest which I admit does not sound as sexy as earning money but I can tell you it is more powerful and I will show you why.

To explain the true value of an offset account and its compounding effects we need to show you in the form of this graph”

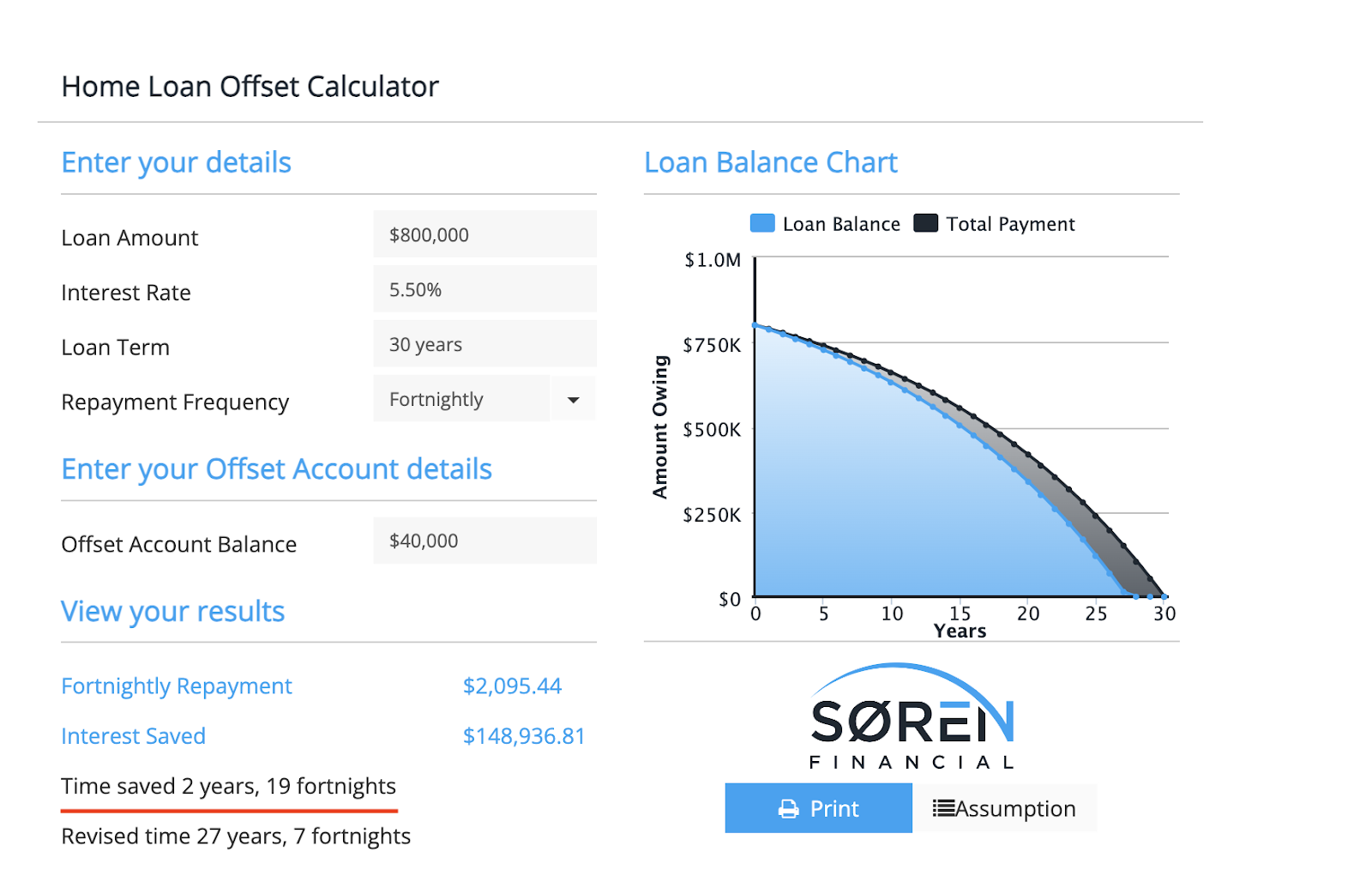

Take a look at what happens when you save up 5% of your loan amount and place it in your offset account under this scenario, congratulations you just cut over two years off your 20 years of your loan, great start!

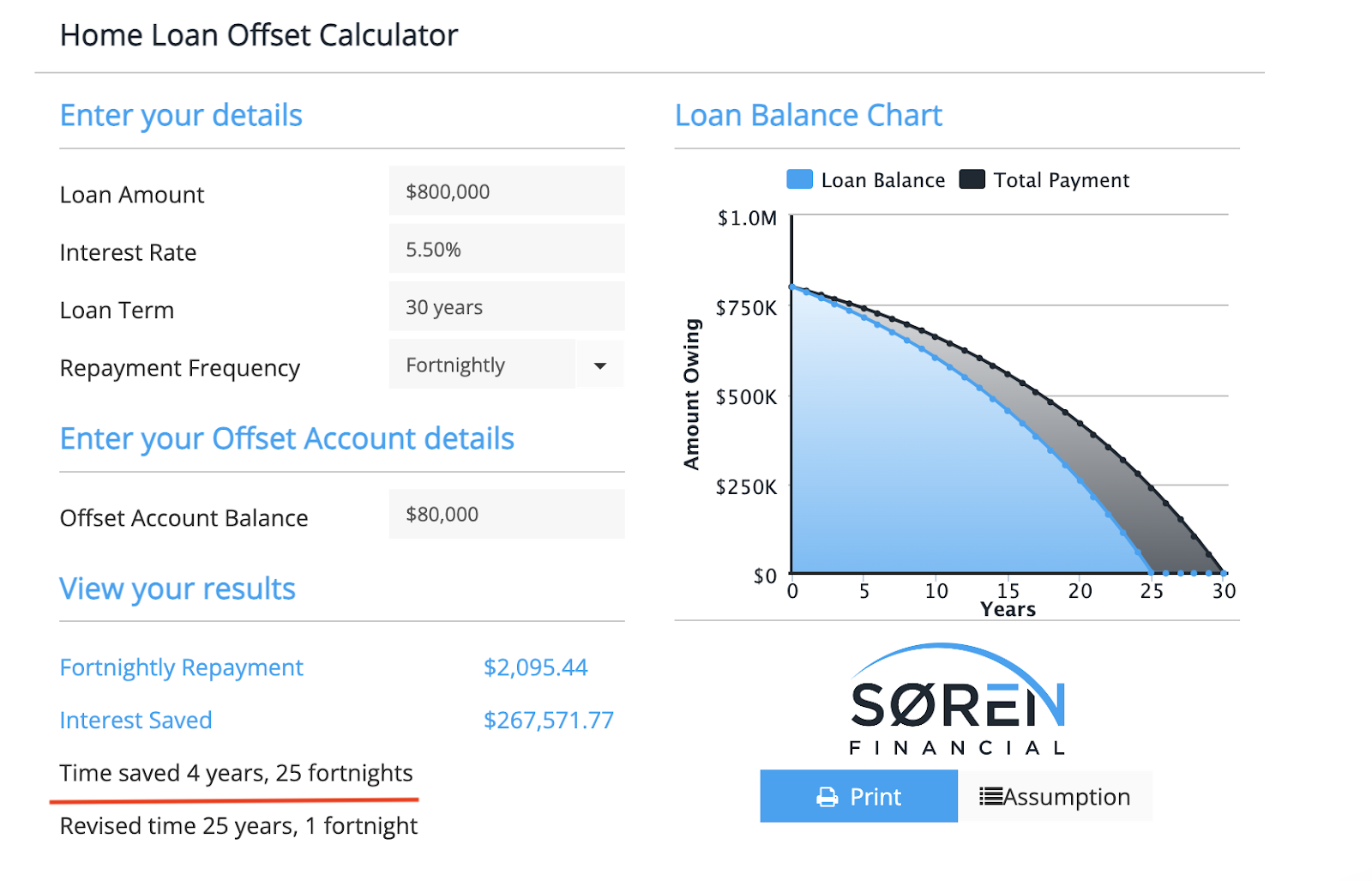

Now look what happens when you save up 10% of the loan amount, you shave off 4.5 years off your home loan. Now think about your situation and what cutting this length of time off your home loan is going to do for your life and the life of your family.

This scenario demonstrates the impact of an $80,000 offset account balance on an $800,000 home loan. Here’s a detailed analysis:

Loan and Offset Details:

- Loan Amount: $800,000

- Interest Rate: 5.50%

- Loan Term: 30 years

- Repayment Frequency: Fortnightly

- Offset Account Balance: $80,000

Results:

- Fortnightly Repayment: $2,095.44

- Interest Saved: $267,571.77

- Time Saved: 4 years and 25 fortnights

- Revised Loan Term: 25 years and 1 fortnight

The amount of money that you save in interest is over 250k however shaving 4.5 years off the loan and the investment opportunities this allows you so you can secure your financial future is huge!

Here are some graph insights:

- Loan Balance: The blue area represents the loan balance over time without an offset account.

- Total Payment: The black line indicates the total payment over time.

- Impact of Offset: With the offset account, the loan balance decreases faster due to the interest savings, as evidenced by the steeper decline of the blue area compared to the black line.

Redraw accounts:

Redraw accounts have the same main advantage that offset accounts have which is they will reduce your overall interest bill. The redraw is there to give you the ability to make extra payments and access those payments whenever you need it.

Redraw accounts are traditionally free with your home loan and the extra funds are meant to be easily accessible (make sure you check this with your lender or mortgage broker before you sign your loan documentation).

We generally tell clients that a redraw account is best for owner occupiers and offset accounts are best for investment property loans unless they specifically request otherwise. Mansour Soltani – Finance Broker

A summary of the difference

Description:

An offset account is a transaction account linked to your home loan. The balance in this account offsets the balance in your home loan, reducing the interest you pay.

Redraw Account

Description:

A redraw facility allows you to make extra payments on your home loan and access those extra funds if needed.

Differences

- Offset Account: Reduces the loan balance daily with the offset balance.

- Redraw Account: Allows withdrawal of extra repayments made.

FAQs

1. What is an offset account?

- An offset account is a transaction account linked to your home loan. The balance in this account reduces the amount of your home loan on which interest is calculated, thus saving you interest over time.

2. How does an offset account help save on interest?

- The lender calculates your home loan interest based on the loan balance minus the balance in your offset account. This means the more money you keep in your offset account, the less interest you pay.

3. What is a redraw facility?

- A redraw facility allows you to make extra payments on your home loan and withdraw those extra funds if needed. It helps in reducing the principal amount of your loan, thereby saving on interest.

4. How does a redraw facility save on interest?

- By making extra payments, you directly reduce your loan balance. The interest is then calculated on this lower balance, resulting in interest savings. You also have the flexibility to access these extra payments if needed.

5. Which is better, an offset account or a redraw facility?

- Both offset accounts and redraw facilities help reduce the interest you pay on your home loan. The choice depends on your financial situation and preferences. An offset account provides easier access to your funds, while a redraw facility requires you to make extra payments that you can withdraw later.

6. Can I have both an offset account and a redraw facility?

- Yes, some lenders offer both options on the same home loan. This allows you to enjoy the benefits of both features simultaneously however please check what the associated costs are.

7. Are there any tax implications with an offset account?

- Unlike interest earned on savings accounts, the interest savings from an offset account are not considered taxable income, which can be a tax-efficient way to reduce your home loan interest.

8. Are there fees associated with using an offset account or redraw facility?

- Some lenders may charge fees for maintaining an offset account or using a redraw facility. It’s important to check with your lender about any potential fees.

9. How much can I save with an offset account?

- The savings depend on the balance maintained in the offset account. For instance, maintaining an $80,000 balance in an offset account linked to an $800,000 home loan at a 5.50% interest rate could save you approximately $267,571.77 in interest and shorten your loan term by 4 years and 25 fortnights.

10. What are the main differences between an offset account and a redraw facility?

- Offset Account: Reduces the loan balance daily with the offset balance.

- Redraw Account: Allows withdrawal of extra repayments made.

11. What is the impact of an offset account on loan term and interest?

- Using an offset account can significantly reduce the interest paid over the life of the loan and can also shorten the loan term. For example, with an $80,000 offset balance on an $800,000 loan, you could save around $267,571.77 in interest and cut 4 years and 25 fortnights off your loan term. Use our offset calculator to see how much you can save by entering your own details.

12. What should I consider when choosing between an offset account and a redraw facility?

- Consider factors such as your need for easy access to funds, potential fees, tax implications, and how each option aligns with your financial goals and habits.